Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

The credit markets of the United States are at their best ever, but Bitcoin finds itself on the verge of new capital – a paradox that sums up the current situation of the digital currency.

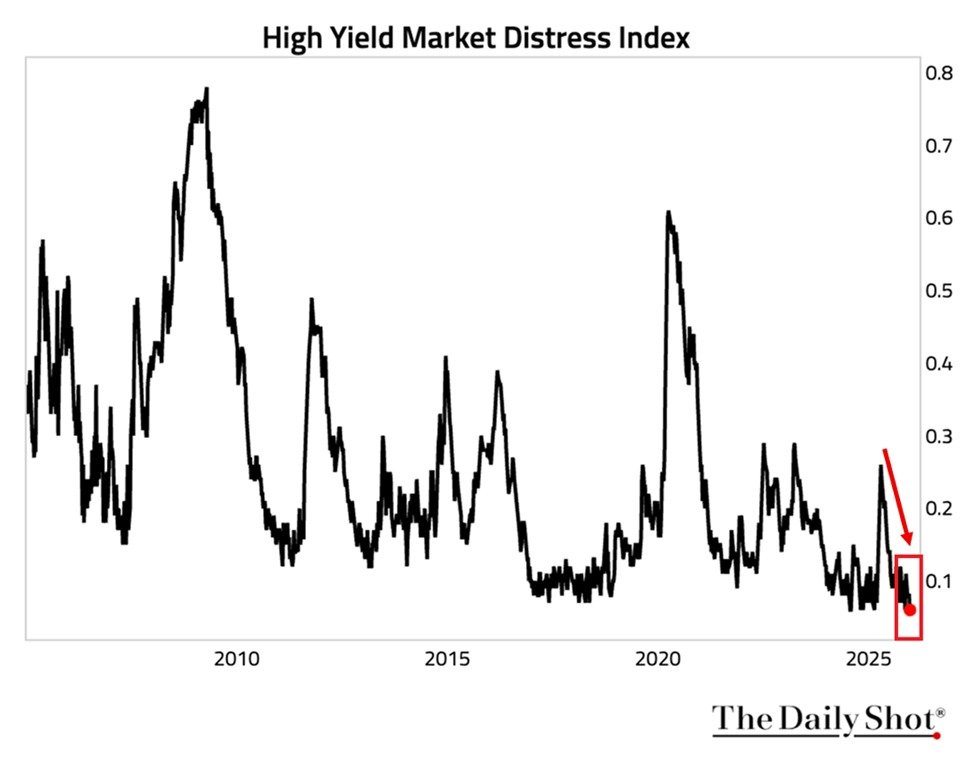

The New York Fed’s High Yield Stress Index recorded Decreased to 0.06 pointsThis is the lowest level in the history of the index. The index measures stress levels in the high-yield bond market by tracking market liquidity, market performance and corporate lending facilities.

Sponsored

Sponsored

To give context, the index exceeded 0.60 during the market turmoil of the 2020 pandemic and approached 0.80 during the financial crisis of 2008. Today’s reading indicates very favorable conditions for the risky asset.

The High Yield Bond Index Fund (HYG) reflects this optimism, extending its growth for the third year in a row with returns of almost 9% in 2025 according to iShares data. According to conventional economic logic, Bitcoin and the rest of digital assets should benefit from this large influx of liquidity and strong appetite for risk.

However, blockchain data revealed a different story. said Ki Young Ju, CEO of CryptoQuant Capital flows in Bitcoin have “dried up”And money moves instead to stocks and gold.

Sponsored

Sponsored

The diagnosis agrees with broader market dynamics. US stock indexes continued to hover near their historic highs. Artificial intelligence stocks and major technology companies represent the majority of capital available for risk. For institutional investors, the risk returns from stocks remain attractive enough to bypass cryptocurrencies entirely.

This contributed to the creation An uncomfortable reality For Bitcoin bulls: Systematic liquidity is abundant, but the cryptocurrency market remains the lowest priority for capital allocation.

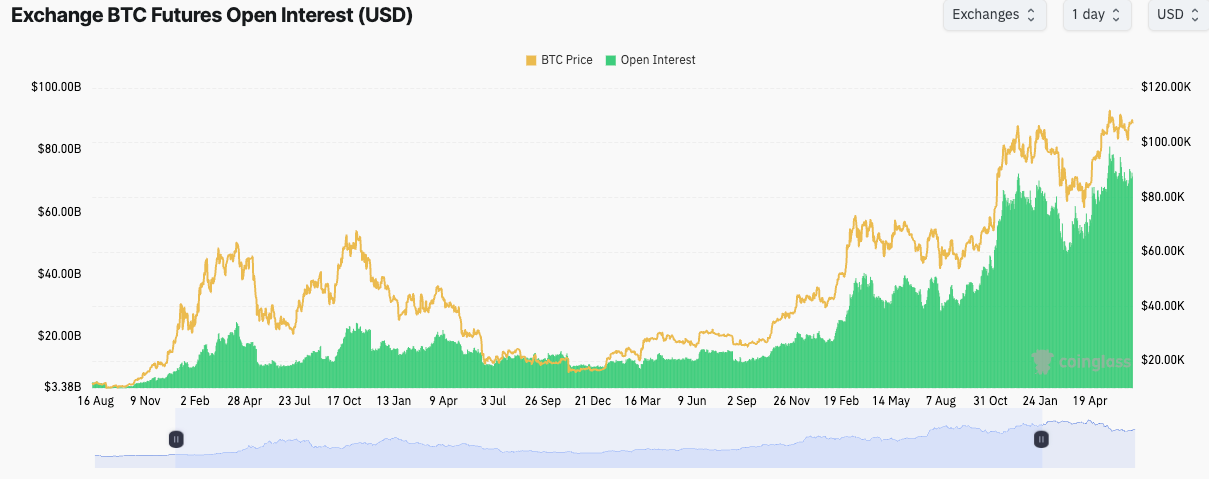

Derivatives data reinforced this recession narrative. Total open interest in Bitcoin futures reached $61.76 billion across 679,120 btc, according to Coinglass. Although open interest increased by 3.04% in the last 24 hours, price action remained in a range near $91,000, with short-term support at $89,000.

Binance led with open interest at $11.88 billion (19.23%), followed by CME at $10.32 billion (16.7%) and Bybit at $5.90 billion (9.55%). The flat distributions on the platforms suggest that the participants are adjusting the hedges rather than building directional conviction.

Sponsored

Sponsored

Note that the traditional sales cycle between whales and retail is also unraveling as institutional holders adopt long-term strategies. MicroStrategy now has 673,000 BTC with no sign of significant selling. Bitcoin spot ETFs have created a new type of patient capital, compressing volatility in both directions.

Key predicted that he does not think we will see a collapse of -50% or more from the historical high like the previous bear markets, just a boring sideways move for the coming months.

Short sellers face weak opportunities in this climate. The lack of panic selling among whales limits the possibility of mass liquidation. At the same time, buyers lack immediate catalysts to drive upward momentum.

Sponsored

Sponsored

Expectations indicate that several potential catalysts could redirect capital flows towards cryptocurrencies: stock valuations reaching levels that prompt investors to switch to alternative assets; A bolder course by the Fed in cutting interest rates increases the appetite for risk; Regulatory clarity gives organizations new entry points; Or specific Bitcoin catalysts, such as changes in supply after the halving and trading options for ETFs.

Until these catalysts are achieved, the cryptocurrency market may be in an extended period of consolidation – strong enough to avoid a collapse, but lacking the impetus for strong growth.

The paradox remains: in a world flooded with liquidity, Bitcoin is waiting for its share.