Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

DASH – the third largest privacy coin by market capitalization after XMR and ZEC – currently faces several risks that many holders may ignore. The positive discussion about privacy coins has taken over the community and may mask these warning signs.

These signals can be important warnings. It may repeat historical patterns, which could cause losses to Dash holders.

Sponsored

Sponsored

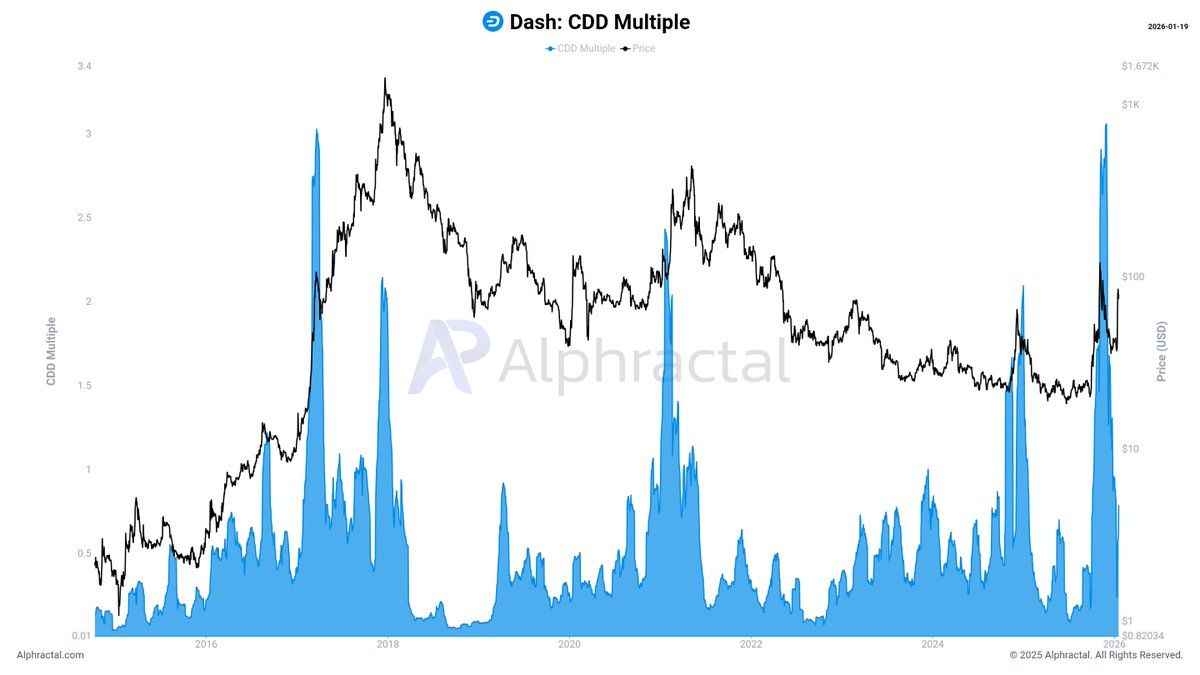

Dash coins that have been dormant for long periods first saw a wave of reactivation in November 2025. These changes indicate a change in the behavior of the holder. A significant reactivation of the old supply often occurs when early investors and long-term holders begin to allocate coins near the top of market cycles.

The Coin Days Destroyed (CDD) indicator measures this behavior. The volume of coins is multiplied by the number of days they have been inactive. When this indicator rises sharply, it often indicates that a large amount of old supplies are returning to the market.

Historically, large CDD rallies have typically coincided with major price spikes in the cryptocurrency markets.

João Wedson said that the long-term coins that were dormant on Dash reactivated significantly in November, but the activity decreased after that. Historically, big moves in long-term passive supply typically occur near the tops of market cycles.

Sponsored

Sponsored

A continued decrease in reactivation activity does not necessarily mean that the risks are decreasing. Distribution phases often last weeks or even months, not just days. This period gives the top holders the opportunity to exit quietly. However, over time, this process can put significant pressure on prices.

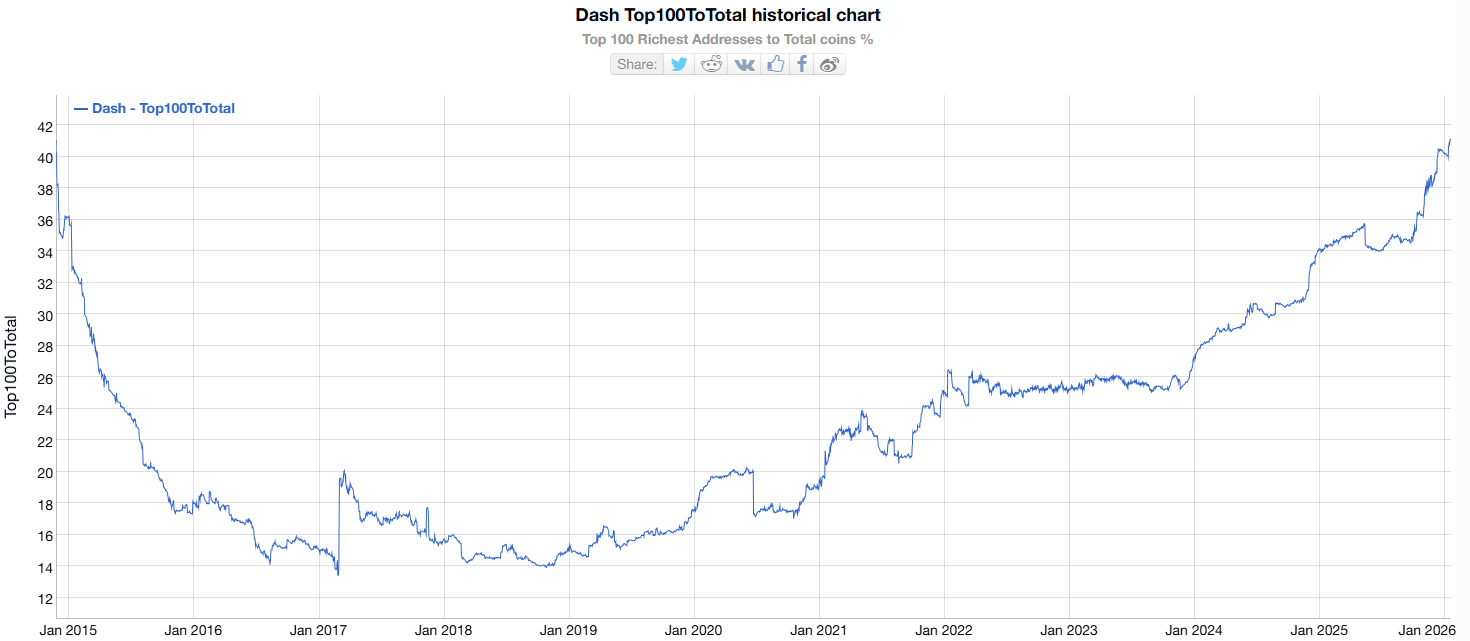

The second risk comes from the increasing concentration of supply. The richest 100 Dash wallets currently control over 41% of the total supply. This represents the highest level in more than a decade, according to Bitinfocharts data.

Sponsored

Sponsored

The graphs show that this share has increased steadily from 15.5%, which was the percentage recorded when Dash reached its maximum in December 2017.

The high concentration of supply can provide stability if large investors remain confident. Principal holders can absorb volatility and commit to long-term positions.

However, this concentration also involves great risk. When a small percentage of addresses control a large part of the supply, their actions can have a big impact on the market. Coordinated or even uncoordinated selling by whales could flood the order books. This could cause sharp downturns and ripple effects in the derivatives markets.

Sponsored

Sponsored

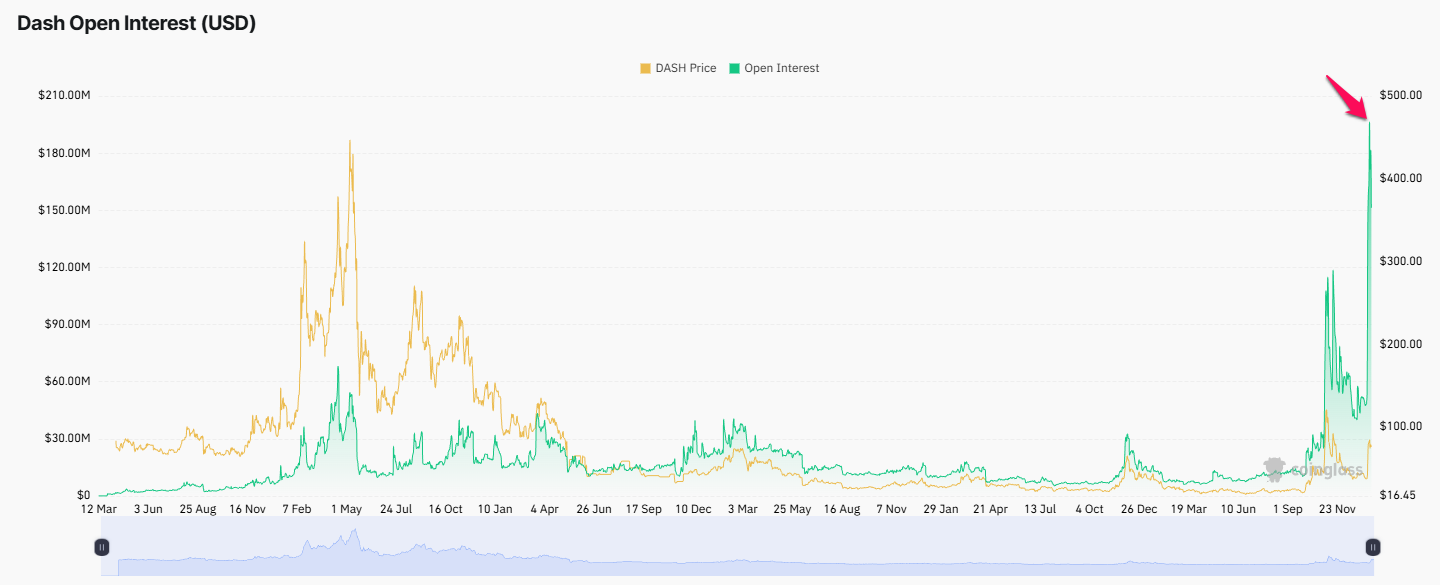

The third risk comes from a growing open interest in Dash in the derivatives markets.

Although Dash is currently trading at about half of its November price, near $150, open interest has risen above $180 million. This represents double the November level, and represents the highest open interest value ever recorded for Dash.

This phenomenon reflects an unprecedented level of leveraged exposure among Dash traders. Such conditions create a fertile environment for massive liquidations. These events can also extend to the spot market.

Additionally, a recent report from PinInCrypto mentioned a shift in capital flows towards low market capitalization private currencies. This phenomenon indicates a decline in investors’ expectations towards large capitalization assets. This may be an additional challenge to DASH’s ability to maintain upward momentum throughout the month.