Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

[ad_1]

Nvidia shares recently set record numbers in the fourth quarter with revenue of $68.1 billion, an annual growth of 73%, and earnings per share of $1.62, smashing estimates. JP Morgan, among others, wasted no time in raising its target price from $250 to $265.

However, on February 26, the stock fell about 7% from its session high of $197 to below $185. The results are undeniable. But price action, money flow and institutional behavior tell a completely different story. At least, for now.

NVIDIA’s Q4 numbers speak for themselves. Revenues reached $68.1 billion, up 73% year-on-year. The data center sector alone generated $62.3 billion, accounting for 91% of total revenue. The EPS (earnings per share) of $1.62 beat the consensus of $1.53 by about 6%.

And fiscal 2027 first-quarter guidance of $78 billion beats Wall Street’s estimate of $72.8 billion — a number that notably excludes any revenue from China.

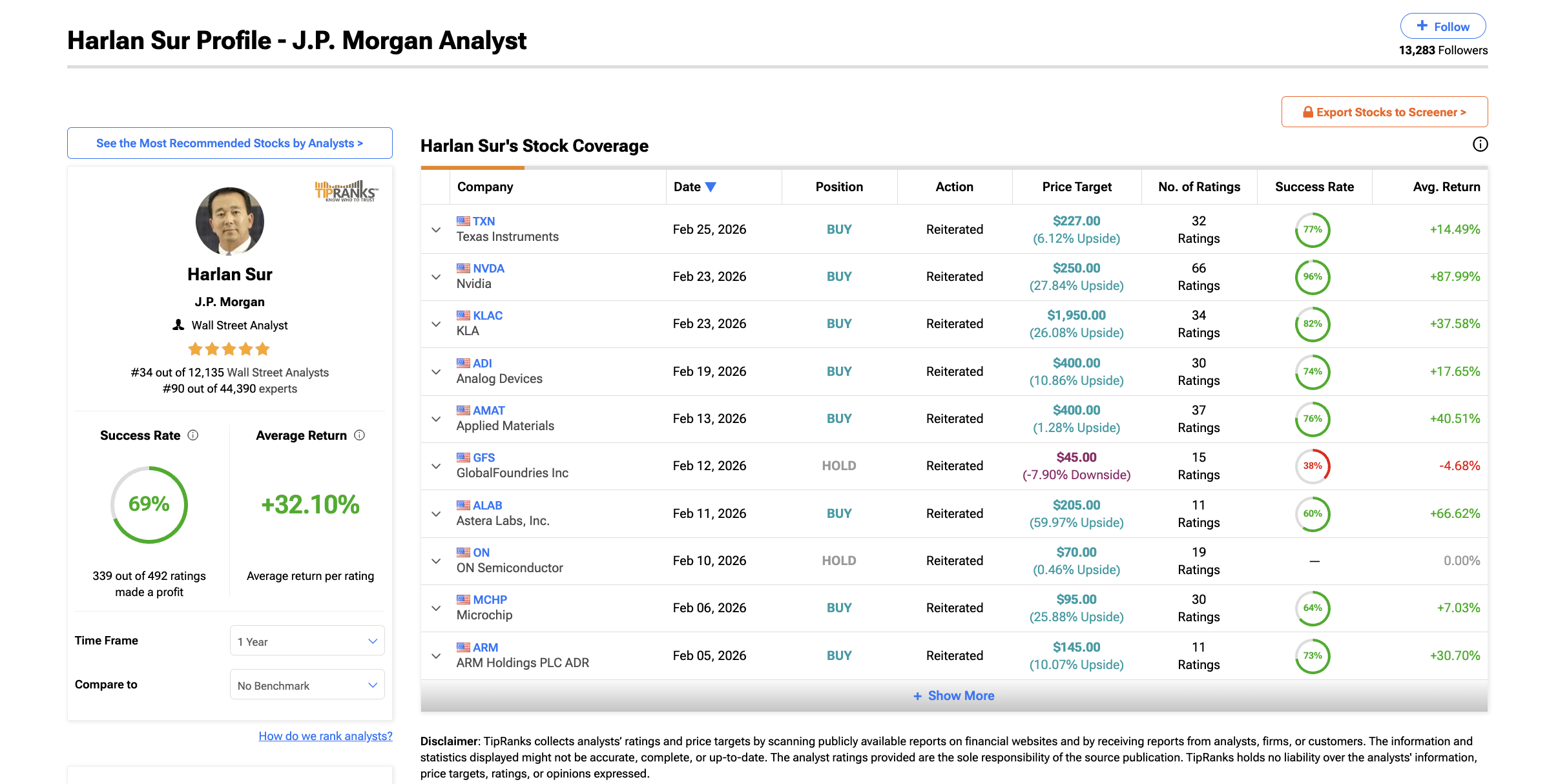

JPMorgan analyst Harlan Suhr responded by raising Nvidia’s price target from $250 to $265.

But here is what most analysts and authorities do not emphasize. NVIDIA’s growth rate on a quarterly basis Slow down quietly. The third quarter grew by 22% compared to the second quarter. The fourth quarter grew by 19.5% compared to the third quarter.

Q1 guidance indicates sequential growth of approximately 14.5%. Revenues continue to break records, but the pace has slowed. For a stock based on growth momentum, this distinction is important. There may be some big money watching.

There is also the question of who actually pays these revenues. Gene Munster of Deepwater Asset Management estimates that about 70% of Nvidia’s revenue comes from just 8 companies.

CFO Colette Kress confirmed that the top 5 hyperscalers (cloud computing providers) account for just over 50% of data center revenues.. This level of customer focus means that even a small decrease of 10-15% In Artificial Intelligence Financial Capital from some big buyers could translate into billions in lost quarterly revenue.

It’s also worth noting that JPMorgan’s asset management division is itself a significant institutional owner of Nvidia.

This is typical of Wall Street, but it is a context that individual investors should be aware of when evaluating the positivity behind a price increase.

Balance Volume (OBV), an indicator that tracks cumulative buying and selling pressure by adding volume over days and subtracting it on down days, tells a positive story on the surface.

OBV has maintained higher levels throughout Nvidia’s 3-month consolidation, indicating continued retail-led buying pressure with continued positivity. However, it still needs to break above the uptrend line resistance to confirm true broad strength.

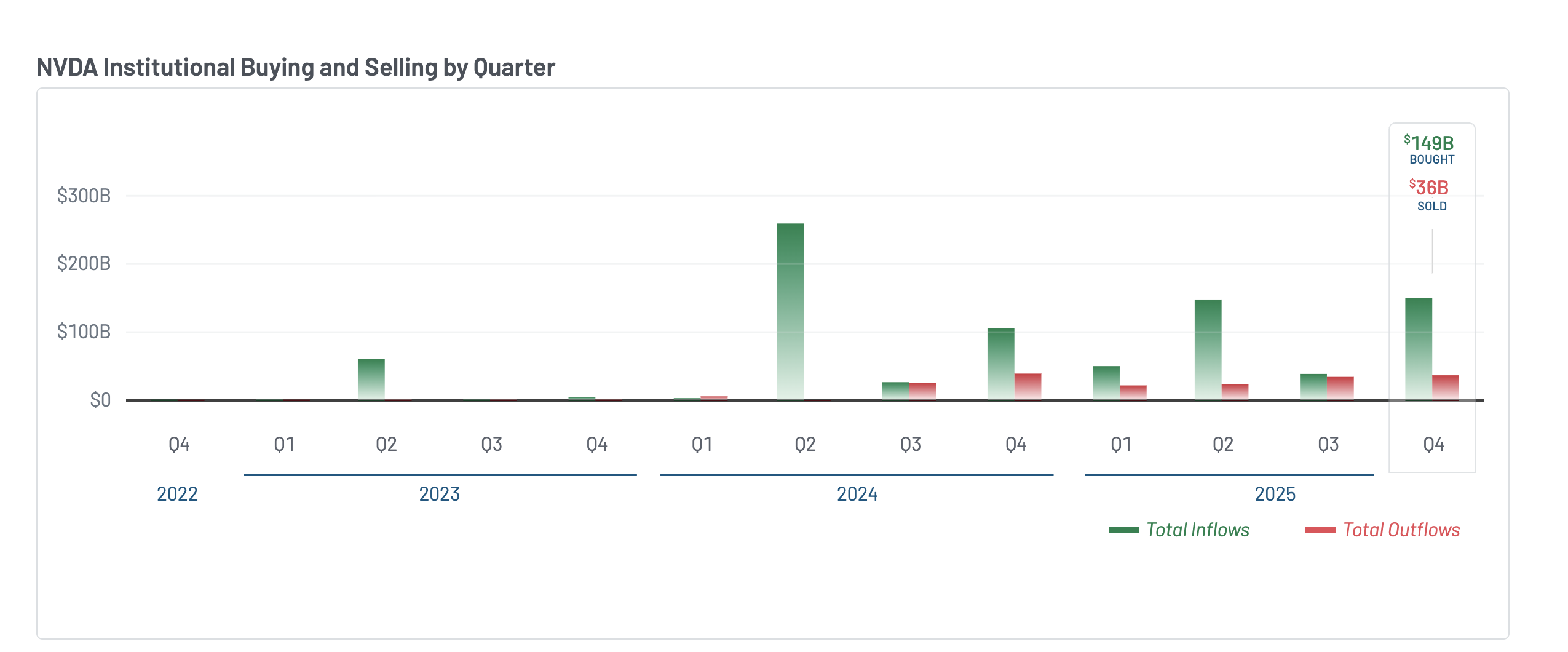

The latest 13F filings (quarterly reports that large investors must file with the SEC to disclose their positions) for Q4 2025 show a dramatic shift in institutional sentiment.

The net outflow of institutional money increased to about $149 billion in purchases versus $36 billion in sales – a net outflow of nearly $113 billion. This is a big improvement over the third quarter, where institutions bought $38 billion and sold $34 billion, leaving a net inflow of just $4 billion.

However, despite this wall of institutional money coming into NVDA in the fourth quarter, the stock market is moving very slowly – trading sideways for most of the period. This suggests that the institutions are accumulating, but the supply from the inside and the previous holders took the demand. NVIDIA CEO Mark Stevens sold it for about $40 million of shares in December.

While Bank of America slightly increased its stake in the stock, it closed both long positions and put the options outright – which neutralized his directional bets.

Institutions are in a clear position. But the coverage and the stable price despite the huge flow suggest that they are onto something. The next section explores what that might be.

The Chaikin Money Flow (CMF) indicator, an indicator that measures whether there is money flowing in or out of a stock based on where the price closes in its volume-weighted daily range, reveals what it isn’t. Earning address .

Since February 5, with the formation of the right shoulder of the inverse head and shoulder pattern in Nvidia, the CMF has always risen with the price. It rose to peak earnings on February 25 when Nvidia briefly touched $197.

Then on February 26, as the stock suddenly reversed to $ 185, CMF fell.

This sudden collapse indicates that the money that entered during the rally was a speculative position – not committed institutional capital – and disappeared the moment the breakout failed. Based on what we discussed earlier, slowing down of revenue may be a reason.

This monthly indicator (VWAP) uses the volume weighted average, which approximates where institutions have built their positions. NVIDIA has traded above the monthly VWAP index since its launch on February 17th.

The last time Nvidia moved away from the monthly VWAP index was on January 30, leading to a correction of about 8.5% in early February.

Since February 26, the stock has fallen below this line. This means that new institutional buyers are now under the surface, which historically leads to more selling as the stop loss is relaxed.

The technical detail has context. Michael Burry noted today that Nvidia’s supply commitments have grown At levels that reflect Cisco before the collapse of the dot-coms – a company that lost billions of dollars when demand was not expectations.

CFO Chris acknowledged that Nvidia has locked up “more than used” inventory. The likes of BofA’s Vivek Arya argue that this ensures Nvidia’s dominance. But the collapse of CMF and the breakdown of VWAP on the same day indicate that the market is not waiting to find out who is right.

The charts, the money flow and the institutional situation all point to the same conclusion – Conviction has been tested at $195, a level highlighted later in the chart. But first, the risk.

On the daily chart, a hidden bearish fork formed between November 10 and February 25. During this period, NVIDIA’s stock price recorded a higher low, while the Relative Strength Index (RSI), a momentum indicator, recorded a higher high.

It’s a sign that bullish momentum is quietly fading even as the stock remains in its range.

Since the divergence began last November, Nvidia is only between $ 169 and $ 199. It was not able to get out of this consolidation despite several attempts – including a reverse encounter on February 25, which failed in 24 hours.

The Fibonacci extension levels of the pattern now mark what comes next. On the upside, $183 at 0.5 is immediate support. Below, $180 becomes a critical level of 0.382 – a break reveals $170, below the right shoulder, and $169, the head. Those levels will completely invalidate the model.

On the positive side, the neckline at $195 remains a major resistance and a test of conviction. A clean daily shutdown above, which NVIDIA failed to do yesterday, is required to reactivate the model.

This could push it towards the expected target of $226, which is the full head-to-neck measurement.

The next extension to $235 approaches the closest target $265 for JP Morgan. The route is on paper.

But as the flow of money, the hidden bearish divergence, and the rejection of 7% today confirm, this is a market that has yet to be bought.

[ad_2]

Source link