Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

[ad_1]

Cross-border payments between companies in 2026 still pose problems that everyone agrees. However, the daily situation does not change much.

Cut times, brokers, manual settlement, surprise expenses. It is still all too common for a simple international transfer to turn into a days-long exercise in waiting, chasing and explaining discrepancies in records.

In fact, the European Central Bank noted that in 2024, a third of cross-border sales payments took more than one working day to resolve, and in almost a quarter of global roads, I got over it It costs 3%.

Even the G20 roadmap shows how big the gap is. By the end of 2027, the purpose It means that 75% of cross-border bulk payments are calculated within an hour. This is it Ambition.

This is part of the reason why stablecoins keep coming back into the discussion. Settlement during Seconds, 24 hours a day, 7 days a day week, Anywhere in the world, And the fees you didn’t even notice. Let’s go deeper.

Stablecoins They make the most sense when you think of them in the context of payments, rather than cryptocurrencies. In the B2B context, these funds function as digital money. Always-on solution, global reach, and the ability to connect directly to workflows via API.

What makes it interesting is that stablecoins are programmable. Once you treat the dollars as programmable objects, you can start building the treasury logic around them.

Norman Wooding, Founder and CEO For SCRYPTit is based on this last point:

“DeFi returns respond to supply and demand in real time – something structurally different from traditional fixed income. Leading CFOs already know: While price pressure continues, stablecoins provide sources of diversification and returns without exposure to crypto prices, or a 1:1 correlation with traditional solutions. SCRYPT provides institutional access, with risk management integrated into the structure.”

In effect, stablecoins can act as settlement money, with open options for Treasury yields that do not depend on being a long-term digital currency.

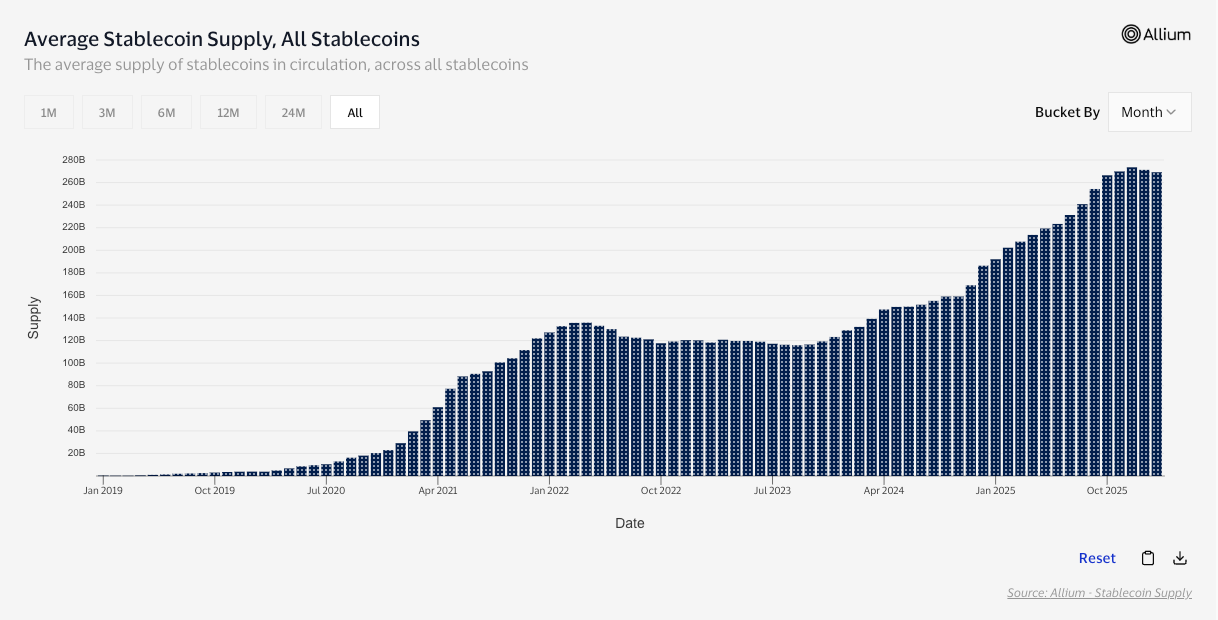

In terms of raw transaction value, the total volume of stablecoins will reach $35 trillion in 2025, according to media reports, citing McKinsey and Artemis Analytics.

But a large volume of chain payments does not necessarily mean large payments. Most of the flow of stablecoins is exchange rebalancing, arbitrage and DeFi routing – an activity that makes economic sense, but is not the same as a business paying a supplier. This is why modified lenses are important. Visa works indicate On chain stablecoins to the volume of transactions an average It reached $10.2 trillion in the last twelve months, with the aim of clearing unpaid transactions.

When you focus on real economic use, the signal becomes stronger. Second To report Stablecoin Payments From Zero to High B2B stablecoin volumes have increased from less than $100 million per month in early 2023 to more than $3 billion by mid-2025, a nearly 30-fold increase.

Therefore, stablecoins transfer their value significantly. Dig deeper into the “why”.

Talk to anyone who moves money across borders for a living, and you’ll hear the same complaints about traditional systems: cut-off times, middlemen, lost taxes and manual settlement.

Stablecoins are a clear gain. They don’t lack middlemen, they operate constantly, they offer low fees and lower rejection rates. In addition, these categories open new audiences for the merchant, positioning them as advantageous and adding a competitive advantage.

It’s not as if the heritage world isn’t trying to catch up. I started SWIFT itself is pushing new rules aimed at predictable cross-border payments for retail, while reducing hidden fees, focusing on full value transfers, and speeding up settlement where local infrastructure allows.

But global coordination is difficult, and so is the G20 program to make cross-border payments cheaper and faster expected It is widely believed that it will not reach its goals by 2027.

Federico Farriola, CEO of Phemex, talks about the adoption curve:

“For younger generations, sending international value via stablecoins already makes more sense than using SWIFT. Traditional bank transfers are slow, complex and expensive, while stablecoins are instantaneous and easier to operate. With regulatory clarity and ease of reporting, there is little structural friction. From a pure money transfer perspective, stablecoins are well positioned for the adoption of traditional systems.

While there is always some friction, there is always some tension. Let’s expand on this.

Recovery must be reliable, liquidity must be under pressure, controls must be auditable, and “what if…” scenarios require solid answers.

Even the IMF’s pro-innovation framework comes with a caveat. Stablecoins can make payments faster and cheaper, but interest diminishes quickly if the market splits into non-interoperable currencies and networks that cannot communicate cleanly.

Central banks are more ruthless. He argues Bank BIS that stablecoins do not achieve the characteristics of basic money (in particular individuality and integrity), which is a polite expression that do not automatically gain trust “without questions”.

The organization is trying to reduce this gap. In the European Union, it integrates MiCA Specific protection for e-money tokens, including rules for issuance and redemption at face value, and the EBA already publishes guidance on redemption schemes, liquidity stress tests and redemption planning. Recommendations The Federal Security Council is pushing in the same direction around the world: consistent standards of oversight, governance and risk management.

Then there is the soft limit: reputational comfort (which is what Farriola pointed out earlier). What is needed now can be a more constructive public narrative so that skeptical users feel at the interaction. For CFOs, this “comfort over reputation” means reduced professional risk.

Stablecoins move their value quickly, every hour, across borders, without the usual chain of intermediaries and delays.

The layer of programmable money is what thickens the plot. Once dollars can be moved, partitioned, and reported as software, use cases for treasury begin to emerge that are not physically possible in the legacy infrastructure of banks. Automated scans, conditional issuance, real-time visibility, and in some cases, policy-driven payment.

Meanwhile, residual friction is real. CFOs are concerned with ensuring recovery, liquidity under stress, auditability, and if the compliance position is defended. Until these boxes are consistently checked, stablecoins will continue to grow as a practical option rather than becoming the ubiquitous default.

But in direction, it is difficult to miss what is happening. Volumes are growing, B2B routes are being created, and mindsets are spreading. The only remaining question is how quickly the layer of conformity and trust will be restored.

[ad_2]

Source link